Overview

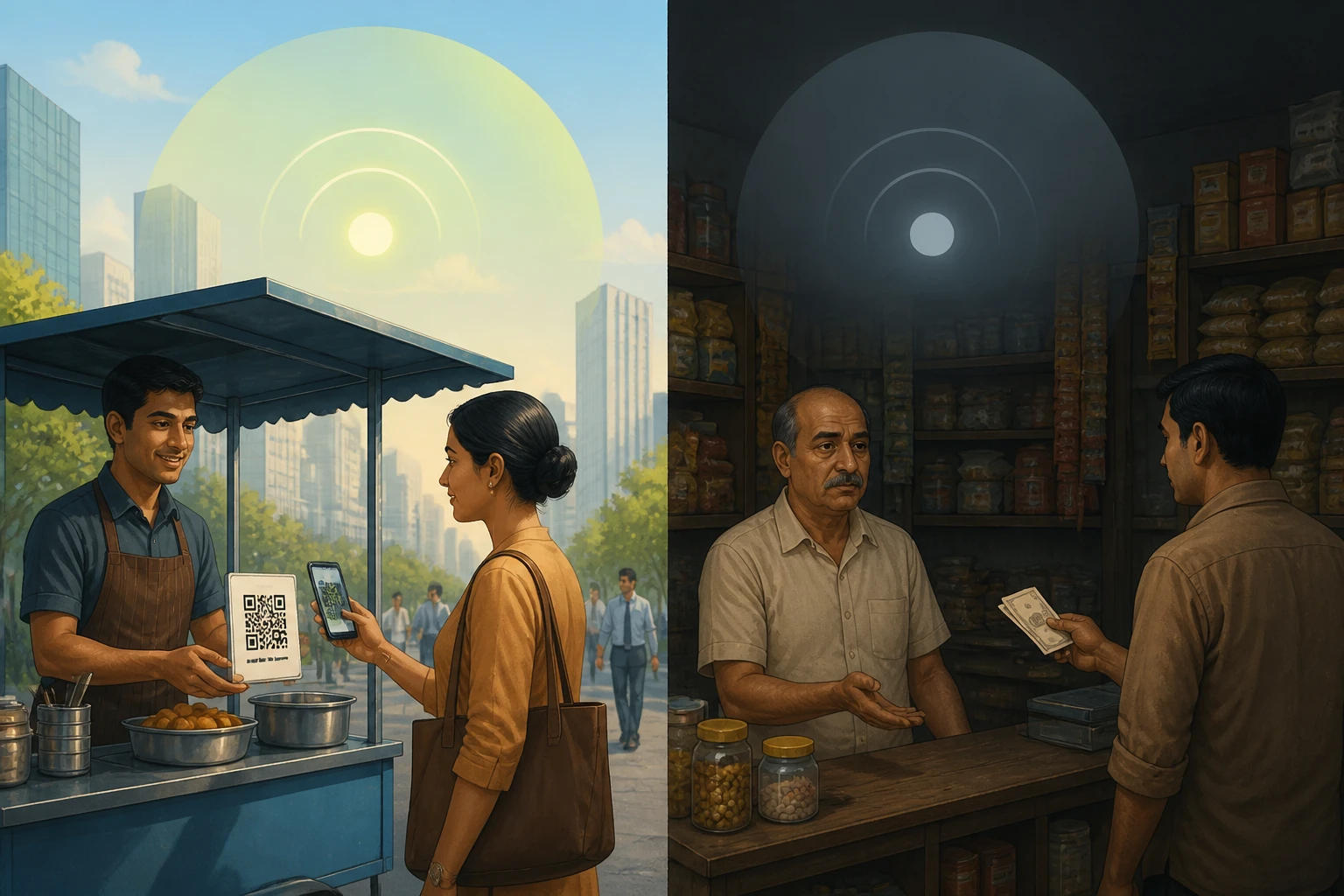

Picture this: You're grabbing your morning dosa from the street vendor outside your office, seamlessly paying with UPI while they cheerfully show off their QR code sticker. But later, when you stop by your neighborhood kirana store for groceries, the uncle behind the counter still insists on cash, dismissing your phone payment attempt with a wave. This isn't just a random occurrence – it's a fascinating digital divide reshaping India's informal economy. While street food vendors are rapidly embracing digital payments, traditional kirana stores are stubbornly sticking to cash transactions. This paradox is creating an unexpected winner-loser dynamic in India's march toward becoming a cashless society, affecting millions of young professionals who depend on both these essential services daily.

The Problem

India recently celebrated crossing 100 billion UPI transactions, yet this milestone masks a peculiar trend: the businesses you'd least expect to go digital are leading the charge, while seemingly obvious candidates are lagging behind. Street food vendors, traditionally operating in the most informal segments of the economy, are adopting UPI payments at rates that would make established retailers envious. Meanwhile, kirana stores – neighborhood grocery shops that serve as the backbone of Indian retail – remain surprisingly resistant to digital payment adoption.

This isn't just about payment preferences; it's about a fundamental shift in how India's informal economy operates. According to recent data, over 60% of street food vendors in major cities now accept UPI payments, compared to just 35% of traditional kirana stores. This digital divide is creating friction in daily urban life, forcing consumers to navigate an increasingly complex payment landscape where cash and digital coexist uneasily.

Analysis

The reasons behind this paradox run deeper than simple technology adoption. Street food vendors operate with fundamentally different business dynamics than kirana stores. Their transactions are typically small, frequent, and impulse-driven – exactly the sweet spot for UPI payments. When someone craves pani puri at 7 PM, they're not planning to negotiate payment methods. The convenience factor heavily favors whoever can process payments fastest.

From an economic perspective, street vendors face unique pressures that make digital payments attractive. They deal with constant cash handling challenges – from making change to storing money securely. UPI eliminates these friction points while providing automatic transaction records that help with basic bookkeeping. Additionally, many street vendors are younger entrepreneurs or recent migrants to cities, making them naturally more tech-savvy and open to digital solutions.

Kirana stores, however, operate on different economics. Their higher transaction values mean that the small UPI processing costs feel more significant. A ₹5 transaction fee on a ₹20 street food order feels negligible, but the same fee on a ₹500 grocery bill feels substantial to store owners operating on razor-thin margins. Moreover, kirana stores often serve older customer bases who prefer cash transactions and have established credit relationships that digital payments can't easily replicate.

The regulatory environment also plays a role. Street vendors often operate without formal business registrations, making cash transactions actually more complicated for record-keeping. Digital payments provide them with automatic documentation that helps legitimize their operations. Kirana stores, being more established businesses, have existing accounting systems built around cash transactions and view digital payment adoption as an additional complication rather than a simplification.

Real-World Examples

Consider Ravi, a chaat vendor in Bangalore's Koramangala district. After adopting UPI in 2022, his daily sales increased by 30% simply because customers no longer needed to carry exact change. He reports that 70% of his transactions now happen digitally, particularly during lunch hours when office workers prioritize speed over payment method.

Contrast this with Sharma Kirana Store in the same neighborhood. Despite serving the same tech-savvy customer base, owner Mr. Sharma estimates only 15% of transactions happen via UPI. "Customers buying ₹1000 worth of groceries always have cash," he explains. "And I don't want to pay fees on large transactions or deal with settlement delays when I need to restock daily."

Paytm's merchant data reveals this pattern across urban India. Street food categories show 85% YoY growth in digital payment adoption, while traditional retail shows only 23% growth. Companies like Pine Labs report that their POS devices see higher utilization rates among food vendors than among grocery retailers, despite the latter having higher average transaction values.

The Challenge

The persistence of this digital divide isn't simply about technological adoption – it's about fundamentally different business models and customer relationships. Kirana stores operate on relationship-based commerce where credit, bulk purchases, and personalized service matter more than transaction convenience. Digital payments can actually disrupt these relationships by formalizing interactions that traditionally relied on trust and flexibility.

Infrastructure challenges compound the problem. While UPI works well for small, quick transactions, larger purchases often involve network timeouts, failed transactions, or daily limits that frustrate both merchants and customers. Kirana store owners report that payment failures on large transactions create customer service headaches that cash simply doesn't have.

Additionally, the tax implications of digital payments create different pressures for different businesses. Street vendors often welcome the formalization that comes with digital records, but established kirana stores may view increased transaction visibility as complicating their existing tax strategies.

Future Implications

This divergence is reshaping urban consumption patterns in ways policymakers didn't anticipate. Young professionals are increasingly gravitating toward vendors who accept digital payments, creating a competitive advantage for tech-savvy street food entrepreneurs while potentially marginalizing traditional businesses that resist change.

The policy implications are significant. Government digital payment incentives designed to formalize the economy are working, but not uniformly. Street food vendors are getting formalized and integrated into the digital economy, while traditional retail remains fragmented between digital adopters and cash-only holdouts.

This trend is also creating new market opportunities. Fintech companies are developing specialized solutions for different merchant categories, recognizing that one-size-fits-all approaches don't work. Payment aggregators are offering customized fee structures and settlement terms that address the specific needs of different business types.

For consumers, this means adapting to a hybrid payment ecosystem where digital and cash payments coexist based on merchant type rather than customer preference. The convenience factor is becoming a competitive differentiator, particularly for businesses serving time-pressed urban professionals.

Looking Ahead

India's path to becoming a truly cashless society won't be linear or uniform. Instead, we're witnessing the emergence of sector-specific digital adoption patterns that reflect underlying business economics rather than just technological capability. The question isn't whether kirana stores will eventually adopt digital payments, but whether they'll adapt their business models fast enough to compete with more digitally native alternatives. As e-commerce and quick commerce continue expanding, the digital divide among traditional retailers might determine who survives and who gets disrupted.